Point-of-sale (POS) lending is growing fast — and not just for big-ticket items anymore. Today, businesses across sectors are offering pay-over-time solutions at checkout to meet demand from younger consumers who prefer fixed monthly payments over credit cards. Studies show that offering financing early in the purchase journey can boost conversion rates by 2–3x.

What Is POS Lending?

Consumers are now looking for more creative ways to stretch their dollar than ever before. As a result, we're seeing a rise in point-of-sale lending — or POS lending.

So, what is POS lending?

POS lending is when a merchant offers their clients a pay-over-time solution at the point of purchase. Traditionally, POS lending has been used to help customers pay for big-ticket items like furniture, home renovations, or cars. However, thanks to technological advancements, it is now easier for merchants in all sectors to offer POS financing.

Growing Demand from Younger Consumers

There is also an upward trend in adoption among younger consumers. Millennials today are moving away from credit cards and favoring the transparency of fixed payment plans.

“3 in 5 millennials carry credit card balances month to month, while 45% don’t know the interest rate on their card.”

Merchants, in turn, are seeing a boost in sales, conversion rates, and cash flow from offering POS lending solutions.

Shift in the Customer Purchase Journey

The average consumer today is more informed and savvier than ever before.

Studies show that:

“Around 75 percent of consumers who finance large-ticket purchases decide to do so early in the purchase journey — before the actual purchase.”

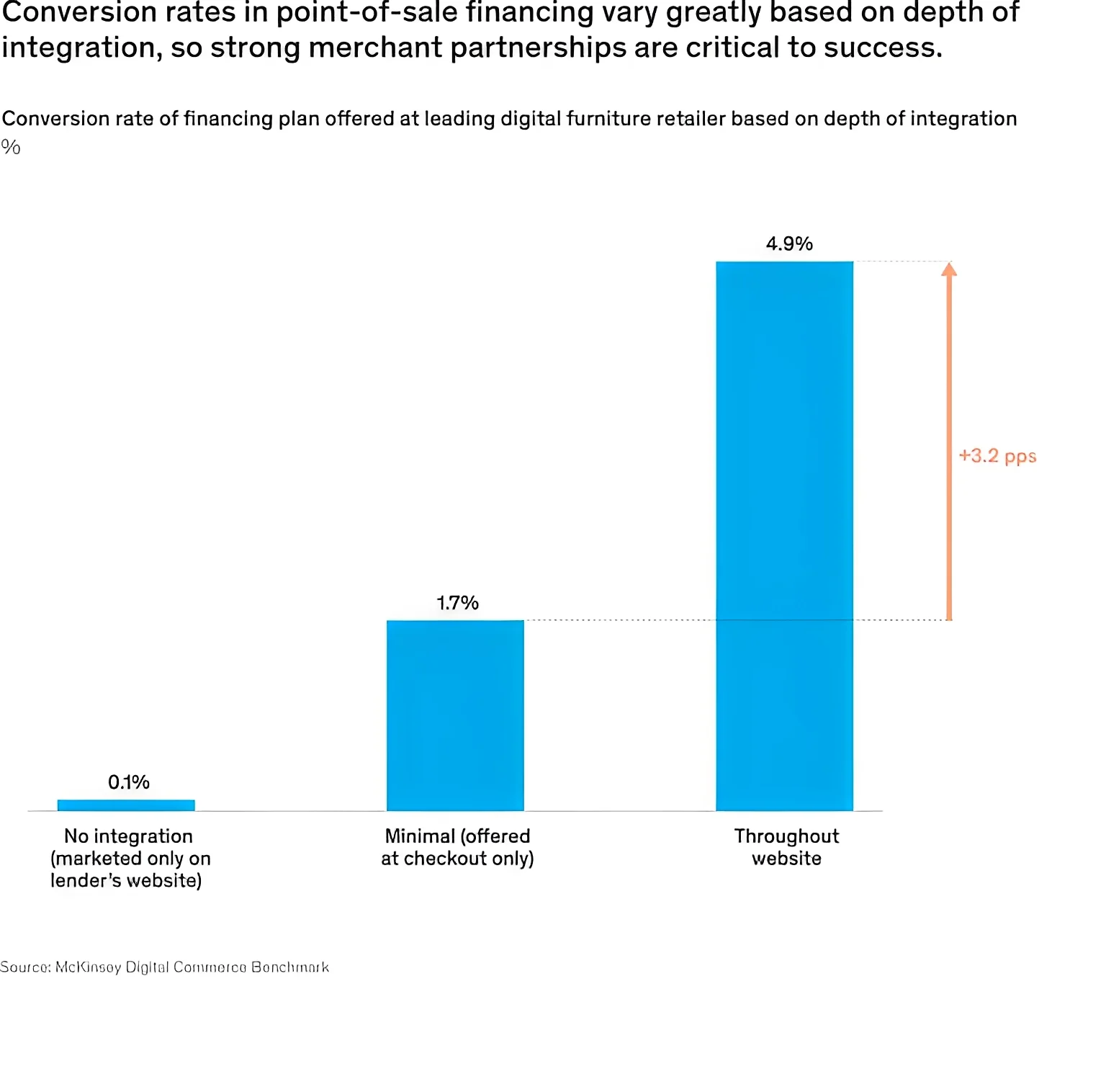

Why Early POS Integration Matters

Merchants who integrate POS lending early in the customer journey are seeing fast success.

Showcasing that you offer payment plans from research to checkout can increase conversion rates by 2 to 3 times, compared to a simple integration at checkout only.

Sources:

https://www.cbinsights.com/research/pos-lending-payments-trends/