- We were recently made aware of a private Sunbit battlecard and accompanying email circulated to practices that contained false and misleading claims about Cherry.

- Below, we address those claims directly — separating marketing language from documented facts so practices can make informed decisions.

Unfortunately, we’ve had to correct the record before.

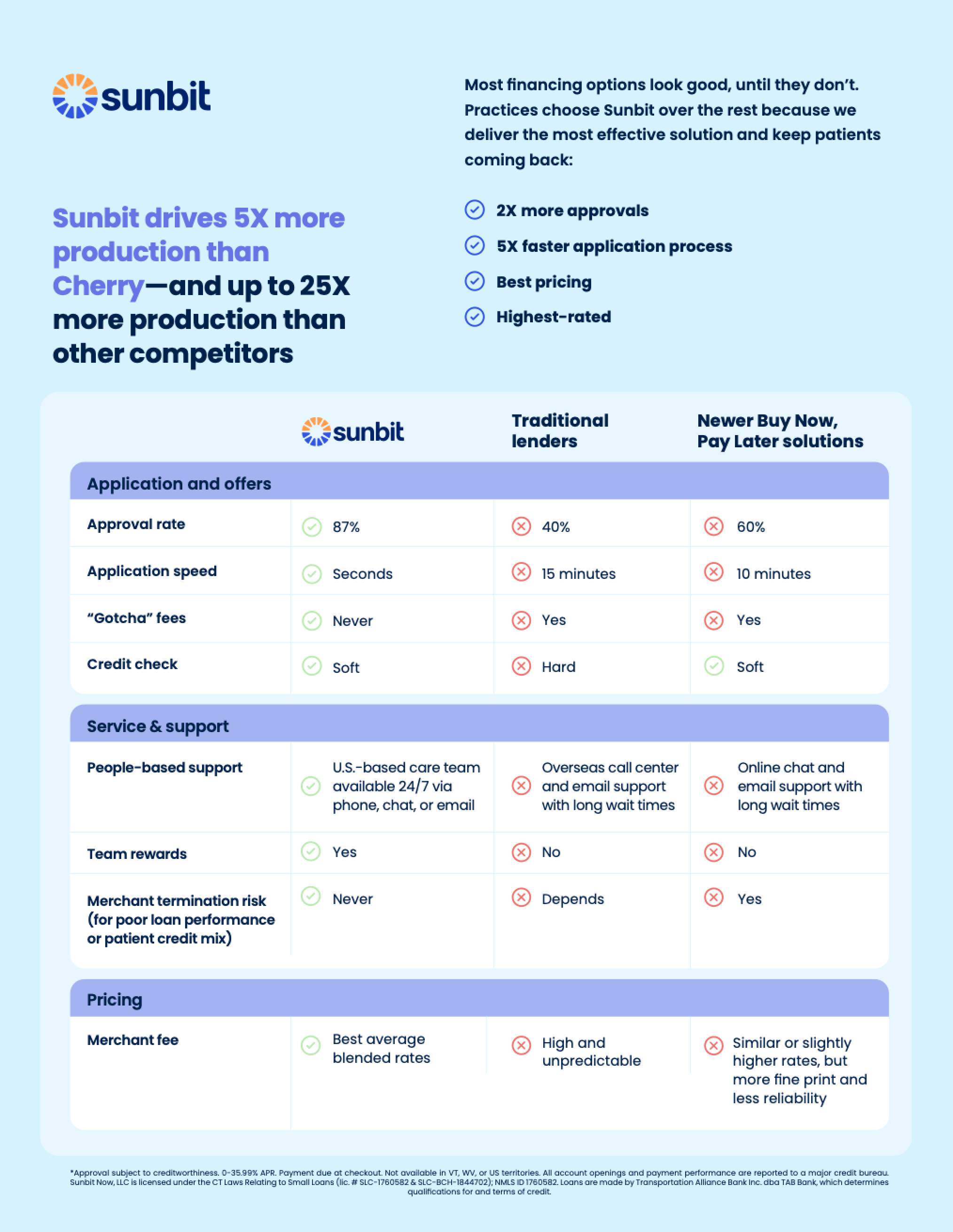

When Sunbit — the auto financing platform that now offers healthcare funding — wants to compete with Cherry, it often does so by publishing comparisons that blur distinctions, stretch language, or rely on selective framing. Recently, we were made aware of a battlecard from Sunbit circulating among dental practices that includes several claims about Cherry that need clarification.

At the very top of that battlecard, Sunbit names Cherry directly. Yet in the comparison grid that follows, Cherry is not explicitly identified. Instead, it appears to be folded into the category “Newer Buy Now, Pay Later solutions” — a classification that conveniently obscures meaningful comparisons in underwriting, pricing, and structure between Cherry and Sunbit.

When information like this is distributed directly to practices, it can’t go unanswered.

Practices are making real financial decisions based on these materials. They deserve transparency — not implication, not marketing jargon, and not category labels that blur the facts.

Before we walk through the claims point by point, here are a few fast facts about Cherry that you’ll see discussed in-depth below:

Cherry was built exclusively for healthcare. Our underwriting, support model, and pricing structure are designed specifically for patient financing — not adapted from another industry.

Now let’s address the claims.

Claim: “Sunbit drives 5X more production than Cherry — and up to 25X more than other competitors”

If a claim sounds fishy or wildly exaggerated, that’s probably because it is. This one is extraordinary, and it’s presented without any cited data, methodology, timeframe, or source.

Here’s the problem: Production depends on a lot of different variables: approval rates, credit mix, merchant fees, patient APR structure, promotional terms, and how financing is positioned in-office. A blanket “5x” or “25x” multiplier without context or documentation is marketing language, not evidence.

If a claim like this had any merit, the data supporting it would be disclosed. It’s not. And here at Cherry, we track a lot of metrics. By no measure that we’re aware of does Sunbit come out as driving “5x more production” than Cherry.

Practices should ask: Compared across what portfolio? Over what period? Using which merchant tiers?

Claim: “Gotcha fees: Never”

“Never” is a powerful claim in lending. It signals certainty: No conditions. No fine print. No scenarios where the opposite could apply.

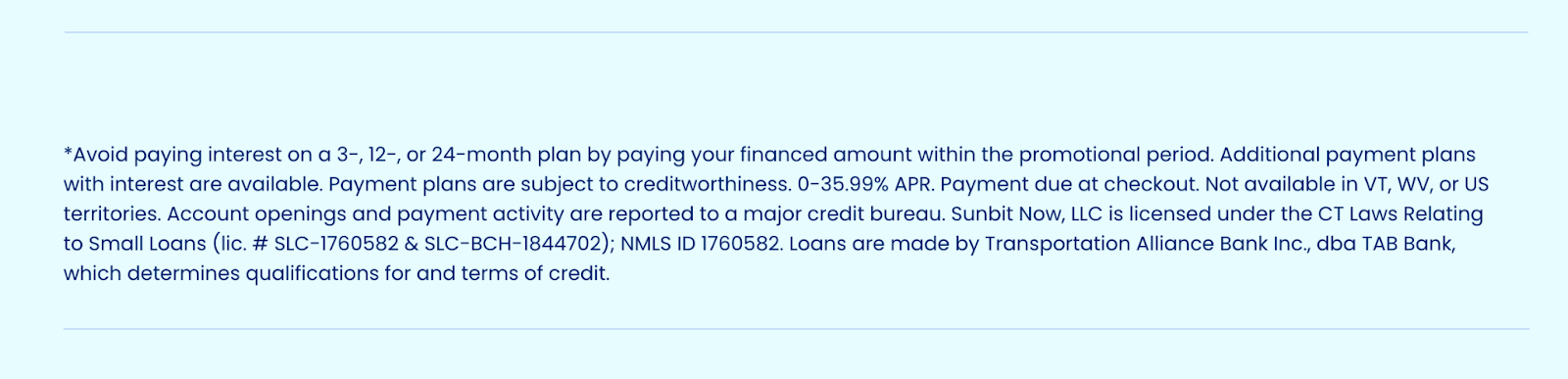

After our original article outlined Sunbit’s use of deferred interest promotions, the term “deferred interest” disappeared from their rates and terms page. The language changed, but the structure didn’t.

Sunbit now markets certain plans as “Avoid Paying Interest,” which is defined on their rates page as this:

That means, under these plans, interest is accruing from day one.

If the borrower pays off the full balance within the promotional window, the accrued interest is waived. If they don’t, that interest becomes due retroactively from the purchase date. What Sunbit is describing is a structure that has long been known in lending as deferred interest — regardless of what they disguise it as now.

At best, it’s misleading to promote financing programs like these — which regulators and entities like the Consumer Financial Protection Bureau have long warned about — with the words “Gotcha fees: Never.”

At worst, it’s deceptive.

Both practices and patients deserve clarity about whether interest is truly not accruing — or simply accruing conditionally behind the scenes.

Changing the terminology doesn’t change the math. When in doubt, look for asterisks and read the fine print:

On this page marketed to practices, you’ll still find both lurking. And that asterisk on “no interest plans, now up to 24 months”? It corresponds to this deferred-interest language at the bottom of the page:

Cherry, on the other hand, has no “gotchas.” Our terms, fees, and rates are clearly disclosed to patients before they borrow. And we never, ever use deferred interest. That’s not because we’ve disguised it using a new phrase like “avoid paying interest” — It’s because we don’t feel it’s transparent or responsible, and it can lead to surprise debt and damaged trust.

Claim: “2X more approvals” (87% vs. 60%)

This one looks precise, and that’s intentional.

In Sunbit’s battlecard, Cherry is grouped under “Newer Buy Now, Pay Later solutions” and assigned a 60% approval rate.

That figure is then used to support the claim that Sunbit delivers “2X more approvals.”

Here’s the issue: there’s no source. No timeframe. No credit mix. No explanation of how that 60% number was calculated.

The truth is Cherry approves up to 90% of borrowers across credit profiles — the highest in the industry. If Sunbit is claiming otherwise, we’d love to see the data behind it. Until then, the 60% figure seems to exist only in their comparison grid.

Approval rates aren’t abstract marketing statistics. They depend on underwriting standards, merchant participation, and the credit profile of the patients applying. Without apples-to-apples methodology, percentage comparisons don’t mean much.

If you’re going to claim “2X more approvals,” the math should be transparent. But transparency is something that Sunbit struggles with.

Claim: “5X faster application process”

Cherry’s application takes 35 seconds and delivers an instant decision at the point of care.

So let’s do the math.

If Sunbit’s application is truly “5X faster,” that would mean it takes roughly 7 seconds to complete. Seeing a trend here? Sounds fishy again, and wildly exaggerated. Because it is.

No application is that fast. It also raises a more important question: How exactly could Sunbit be making an informed decision about eligibility so quickly?

Responsible lending requires collecting and assessing meaningful information about a borrower’s financial situation. That protects the patient. It protects the practice. And it protects the integrity of the portfolio.

Speed is important. But speed without substance isn’t a virtue.

If a lender is approving patients in a matter of seconds — dramatically faster than industry norms — practices should ask what data is being reviewed, how underwriting decisions are being made, and whether that process is built for long-term sustainability.

A fast application is helpful. An incomplete one is not.

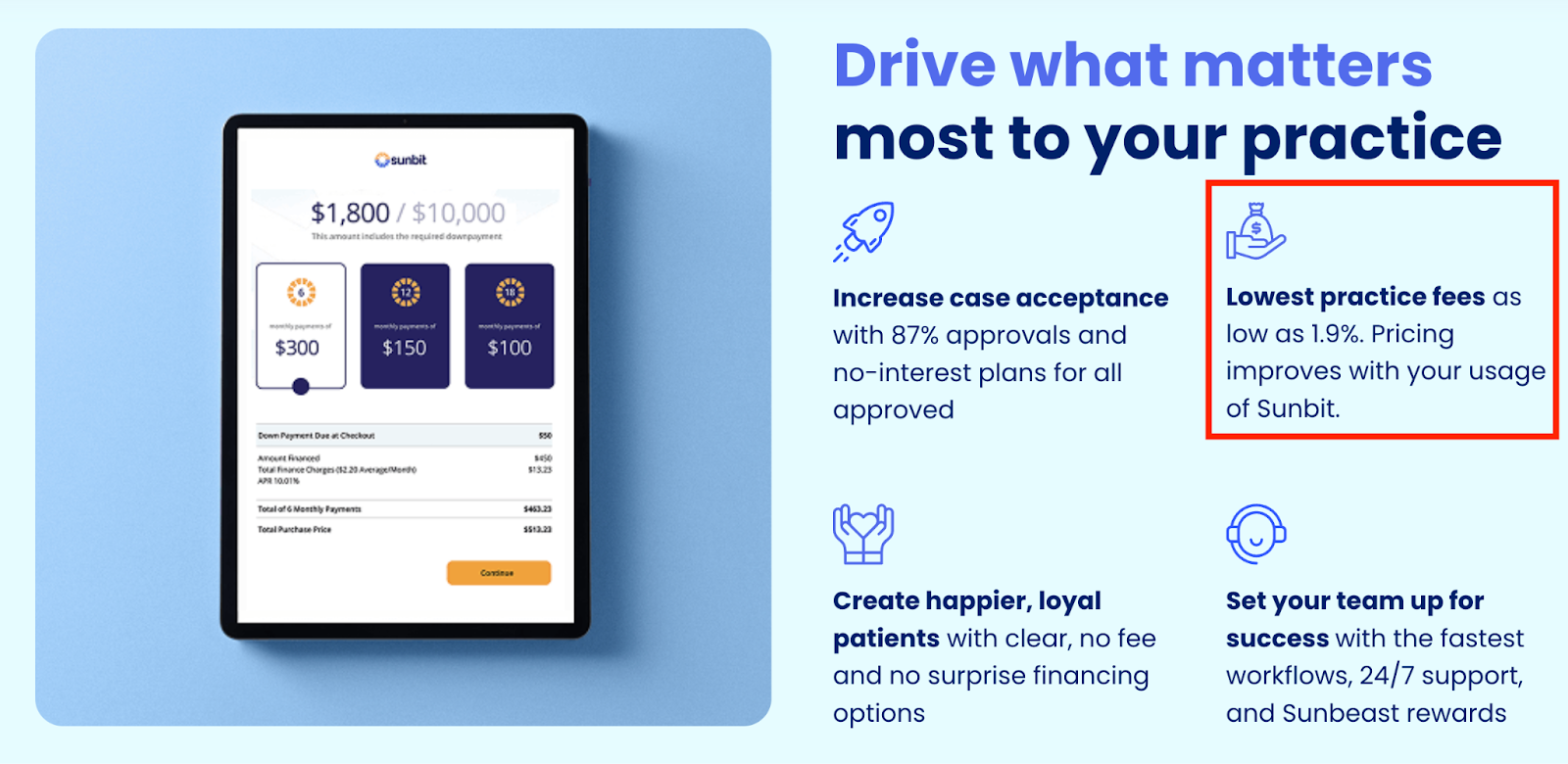

Claim: “Best pricing” / “Best average blended rates”

Let’s start with something straightforward.

Sunbit advertises merchant fees starting at 1.9%. Cherry’s merchant fees start at 1.7% or 1.9% depending on the industry.

It’s basic arithmetic. 1.7% is lower than 1.9%. That means Cherry’s lowest fees are the same or better than Sunbit’s. We’re not sure where the confusion is.

Now let’s talk about the phrase “best average blended rates.”

“Blended rates” is a conveniently vague term. Blended across what? Which credit tiers? Which promotional structures? Over what volume mix?

When pricing needs to be blended to look competitive, that should raise questions.

Cherry doesn’t blend rates. We’re clear and up front about pricing. There are no subscription fees, no annual fees, no equipment costs, and no setup charges. We charge one thing: a merchant fee per transaction — and it’s the lowest in the industry.

No bundling, blending, or math gymnastics.

If a company needs to rely on undefined averages to claim “best pricing,” practices should ask to see the underlying breakdown. Because in financing, clarity beats clever phrasing every time.

Claim: “Merchant termination risk (for poor loan performance or patient credit mix): Never”

Sunbit claims there is “never” merchant termination risk tied to loan performance or patient credit mix.

That framing does more than describe their own policy. It implies that other lenders terminate merchants for performance or credit mix.

That’s a serious allegation. And once again, no evidence is provided. No examples, documentation, or data.

If widespread merchant termination for loan performance were common across the industry, it would be easy to cite proof. Sunbit doesn’t. Not here, or anywhere else on this battle card.

Repeatedly, we’ve seen exaggerated multipliers, undefined “best” pricing claims, absolute language like “never,” and comparisons that blur meaningful distinctions. And this isn’t the first time.

They’ve previously made up data they can’t support; implied that being transparent with applicants is bad for business; and even created a whole new term for deferred interest to avoid its negative associations (see “Avoid Paying Interest” terms above).

At some point, the issue isn’t the claim itself. It’s the pattern.

Practices shouldn’t be asked to accept bold accusations about competitors without documentation. That’s not how responsible comparisons are made.

Credibility matters.

And when a company repeatedly asks you to take its word for it, that’s worth noticing.

Claim: “People-based support” (24/7 U.S.-based care team)

Sunbit advertises 24/7 U.S.-based phone, chat, and email support, while suggesting other leading BNPL programs offer only chat and email. Let’s clarify something:

Cherry offers help via email and chat, and real, people-based phone support through a U.S.-based customer support team. Our hours are 9AM–9PM Monday-Friday, and 9AM–6PM on Saturdays. We don’t operate on Sundays.

We’re transparent about that.

Now here’s what practices should consider.

Providing fully staffed, truly live, U.S.-based phone support 24 hours a day, 7 days a week is resource-intensive. It requires overnight shifts, multi-time-zone staffing, and significant operational overhead.

It’s not impossible, but it is uncommon. So, when you see “24/7 support,” it’s worth asking what that actually means.

Does it mean a live U.S.-based representative answers the phone at 3:00 AM? Or does it mean you can submit an email or chat request at any time — and receive a response during standard business hours?

There’s a difference.

Cherry doesn’t stretch definitions to win a comparison chart. We clearly state our hours, staff our team responsibly, and provide real human support when practices and patients need it.

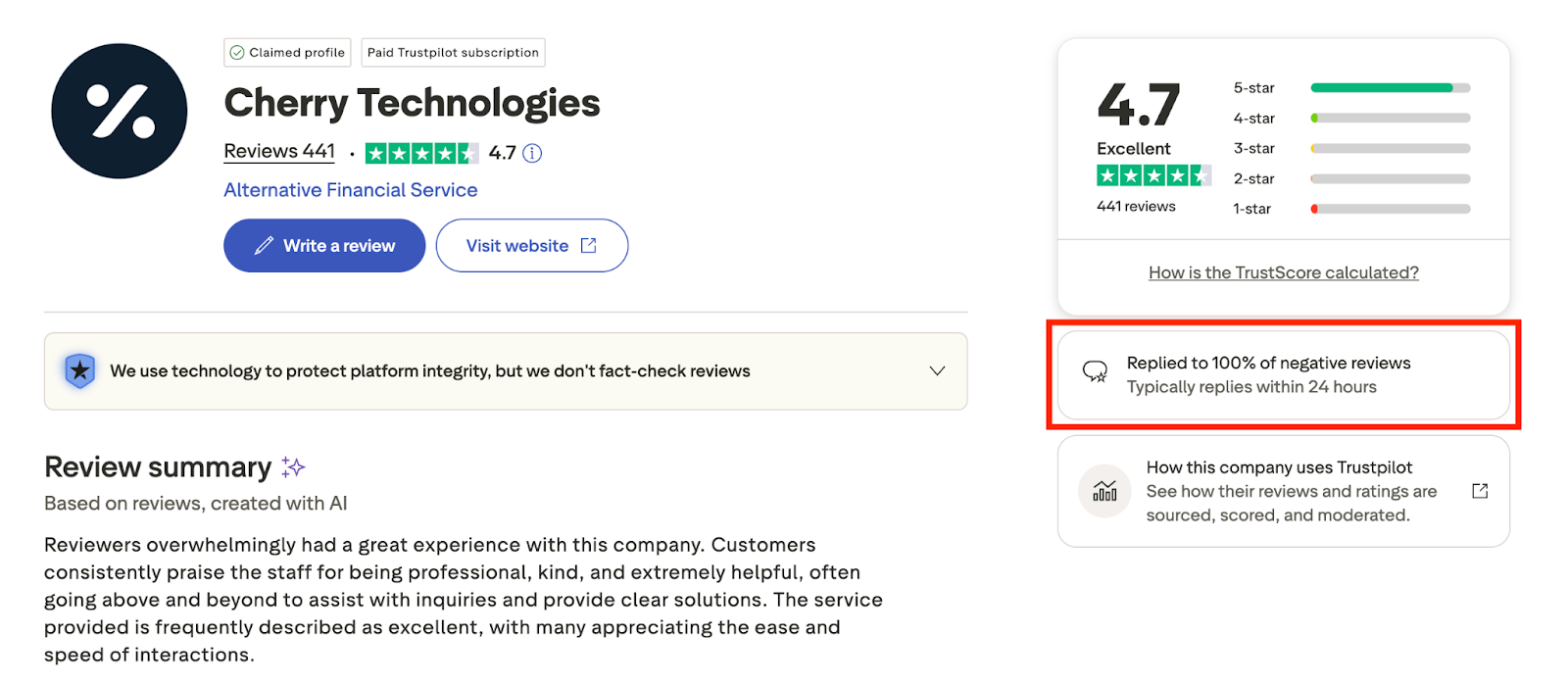

Claim: “Highest-rated”

Sunbit’s battlecard describes itself as the “highest-rated” financing company.

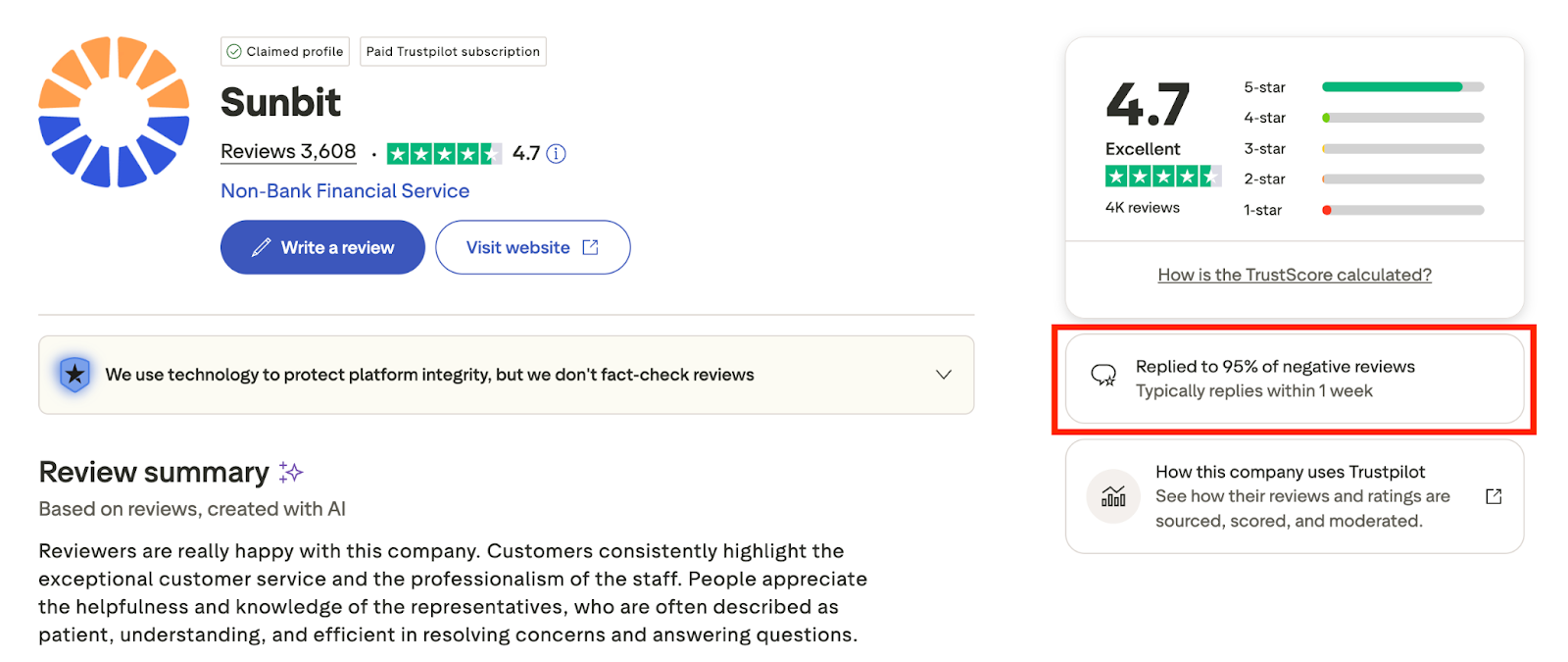

According to Trustpilot, both Sunbit and Cherry currently hold a 4.7-star rating. So “highest-rated” compared to whom?

If both companies carry the same public rating, the claim doesn’t reflect a measurable distinction. Now let’s look a little deeper.

Trustpilot also tracks responsiveness to negative reviews. Cherry has responded to 100% of negative reviews — typically within 24 hours.

Sunbit, on the other hand, responds to only 95% of negative reviews — and typically within a week.

That may not seem dramatic at first glance. But responsiveness matters — especially when a company is simultaneously marketing 24/7, round-the-clock, U.S.-based support.

If a lender is truly operating at that level of availability, you would expect response times to reflect it, particularly in public-facing customer concerns.

Ratings matter. But responsiveness says just as much about how a company supports both its practices and borrowers.

Practices should look beyond the headline claim and examine how consistently and how quickly a financing partner engages when issues arise.

The Bottom Line

Financing is built on trust. When a company relies on undefined averages, selective statistics, and absolute claims that don’t hold up under scrutiny, practices should pause.

Healthy competition doesn’t require stretching numbers. It doesn’t require blurring distinctions. And it certainly doesn’t require rewriting terminology while keeping the same mechanics in place. So here’s the question that matters:

Can you confidently partner with a company that has to cherry-pick comparisons and lean on questionable claims to win your business?

Cherry was built exclusively for healthcare. We compete on transparent pricing, responsible underwriting, real support, and terms that say exactly what they mean. Over 60,000 practices already partner with Cherry to grow their business and expand access to care. And when both Sunbit and Cherry are available at a practice, Cherry is recommended first to patients 8.8x more often.

If you’re evaluating financing partners, don’t just read the headline claims. Examine the math. Review the agreements. Ask how the numbers were calculated.

For us, trust isn’t a marketing buzzword. It’s the foundation of our relationship with our partners. And when you succeed, we do too. To learn more about how Cherry can help you transform your practice with patient financing, claim your personalized demo here.